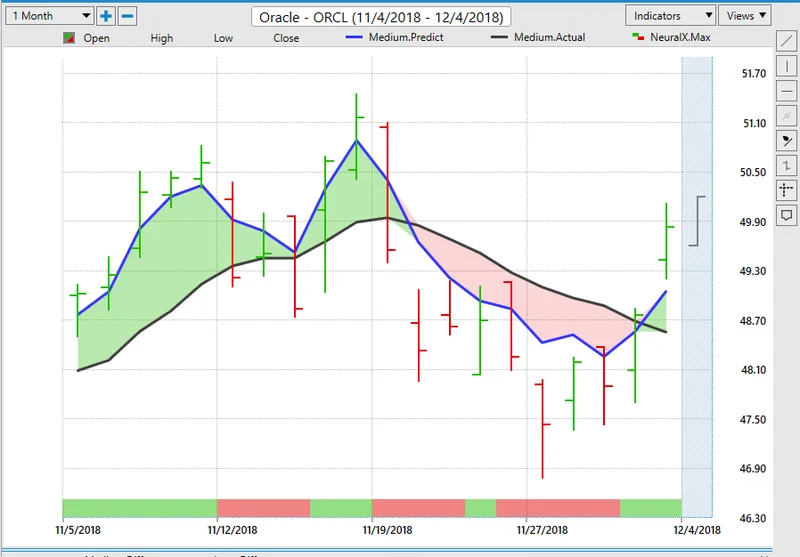

Alright, let's get real for a minute. 'Perfect time,' they say. Always is, ain't it, when the market takes a dump and some analyst with a spreadsheet the size of Texas decides it's actually a secret opportunity. Oracle (ORCL) stock, right? Just had its "implosion," apparently. Thirty percent off the top in a month. Sounds like a fire sale, or maybe a five-alarm dumpster fire, depending on who you ask.

And of course, the usual suspects are out there, pounding the table, screaming about a "contrarian opportunity." Because nothing says "smart money" like buying something after it’s already bled out, hoping it’ll magically reanimate. Give me a break. But this time, it's supposedly different. It's "perfect." And why? Because some high-minded financial wizardry says so.

So, here's the setup for this "perfect time." Oracle missed its earnings expectations for Q1. Shocker. But then, poof, like a magician pulling a rabbit out of a hat, their "remaining performance obligations" (RPOs) shot up to $455 billion. That's a 359% jump from last year, a massive leap. And the reason? Oracle Cloud infrastructure, baby. AI demand. Suddenly, the missed earnings are just a quaint little detail, overshadowed by the shimmering promise of artificial intelligence.

Now, this is where it gets good. The market, in its infinite wisdom, sees this huge RPO number and thinks, "AI! Growth! Future!" But then, in the very next breath, it gets spooked by "AI bubble fears." So, Oracle loses 30% of its value. See how that works? It’s like watching a cat chase a laser pointer – they’re chasing the AI dream, then suddenly afraid of its own shadow. Are these "fears" real, or just a convenient excuse for some folks to shake out the weak hands before they swoop in? I'm just asking, you know... how much of this is genuine market sentiment and how much is just the big players playing chicken with the little guys?

And let's not even get started on the "is it cheap?" debate. Some genius claims ORCL at 37.8x forward earnings is "far from cheap." But then, they immediately follow up with, "if Oracle executes on its AI and cloud initiatives... then it can justify or grow into its valuation." So, it's not cheap now, but it will be cheap if it does all the things they expect it to do in the future? That’s like saying my old beat-up car ain't worth much, but if I put a jet engine in it and make it fly, it'll be a bargain. That's not how valuation works, folks. It’s an assumption, not a demonstration. It's the financial equivalent of Christopher Hitchens asking for proof of divine rights, and these analysts just shrugging, "Trust me, bro." We're supposed to just accept this logic? Honestly, it's enough to make you wanna...

But wait, there's a new sheriff in town, a quantitative one. Forget all that squishy fundamental stuff and past performance charts. We're talking "Kolmogorov-Markov framework layered with kernel density estimations (KM-KDE)." Sounds like something out of a sci-fi movie, doesn't it? It’s a fancy, mathematical way to say they're trying to plot "probability density as a function of price." Essentially, they're looking for when stocks "cluster" under specific conditions.

This is the alleged engine behind the "perfect time." This model, apparently aggregating data since 2019, suggests that after a specific "3-7-D formation" (three up weeks, seven down weeks, overall downward slope in the last 10 weeks – try saying that five times fast), ORCL stock has a projected 10-week return range. And the sweet spot, the "price clustering," is around $212. That's a 1.68% positive variance between baseline and conditional circumstances. Not exactly a lottery win, is it? But enough, apparently, to justify some serious options leverage.

The big play here is a 210/220 bull call spread expiring January 16, 2026. Buy the $210 call, sell the $220 call, net debit of $435. Maximum profit of $565 if ORCL hits $220. Breakeven at $214.35. They say it's "aggressive" but "still rational." Rational for whom, I wonder? For the folks who understand what a "net debit" and a "second-leg strike" actually mean, or for the average schmo just trying to make sense of why their 401k looks like a rollercoaster? This whole thing feels like trying to catch a snowflake on your tongue while wearing a blindfold. You might get lucky, offcourse, but I wouldn't bet the farm on it.

So, Oracle’s stock "stumble" isn't just a stumble, it's a meticulously calculated opportunity. A "perfect time," if you will, but only for those with the tools, the knowledge, and the stomach for this kind of high-wire act. Wall Street still has Oracle as a "Moderate Buy" with a ridiculous 76% upside potential. Always bullish, those guys. They’ll never tell you to sell, will they?

This whole saga—the market panic, the RPO revelation, the AI hype, the algorithmic "solution"—it’s a masterclass in how narratives are built, torn down, and rebuilt in the financial world. It’s not just about the numbers; it’s about the story the numbers let you tell. And right now, the story is that Oracle’s dip has created a "pricing inefficiency" that can be exploited. It's not about hoping for a bounce back; it's about betting on a very specific, statistically defined bounce. And if you've got the guts and the brainpower to navigate those options, maybe, just maybe, it is your perfect time. Then again, maybe I'm just a cynic who prefers his money in a mattress...